What is a T Account?

A T Account is the visual structure used in double entry bookkeeping to keep debits and credits separated. For example, on a T-chart, debits are listed to the left of the vertical line while credits are listed on the right side of the vertical line making the company’s general ledger easier to read.

Here’s What We’ll Cover:

Why Do Accountants Use T Accounts?

What Are the Problems with T Accounts?

Why Can’t Single Entry Systems Use T Accounts?

Why Do Accountants Use T Accounts?

Accountants use T accounts in order to make double entry system bookkeeping easier to manage.

A double entry system is a detailed bookkeeping process where every entry has an additional corresponding entry to a different account. Consider the word “double” in “double entry” standing for “debit” and “credit”. The two totals for each must balance, otherwise there is an error in the recording.

A double entry system is considered complex and is employed by accountants or CPAs (Certified Public Accountants). The information they enter needs to be recorded in an easy to understand way. This is why a T account structure is used, to clearly mark the separation between “debits” and “credits”.

It would be considered best practice for an accounting department of any business (that is not using a single entry method of accounting) to employ a T account structure in their general ledger.

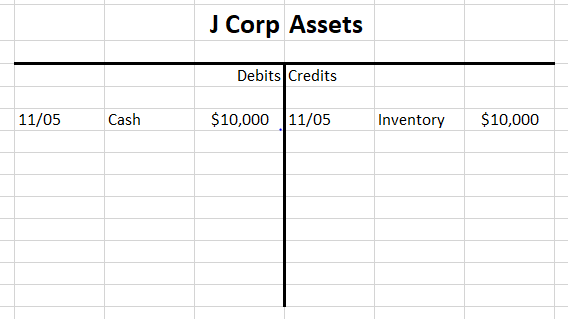

T Account Example

Here is an example of a T Account entry:

This asset entry shows that J Corp has sold a product valued at $10.000. This means the debit account is seeing a $10,000 increase in cash, while the value of its inventory (under “credits”) has been reduced by that same amount.

To fully understand this diagram, consider that:

- Debits increase asset or expense accounts, while credits decrease them.

- Debits decrease liability, revenue or equity accounts, while credits increase them.

They must always balance each other out.

T Accounts always follow the same structure to record entries – with “debits” on the left, and “credits” on the right.

What Are the Problems with T Accounts?

T Accounts are the visual representation of a double entry system of accounting. There are disadvantages to this system, such as:

INFORMATION NOT PROPERLY RECORDED

This can cause a company’s general ledger to not balance. However, since debits and credits are entered at the same time, these kinds of mistakes can be easier to catch if the accountant checks his numbers after every journal entry.

THERE ARE COMPLETE OMISSIONS

This is when a transaction is not recorded at all. These errors may never be caught because a double entry system cannot know when a transaction is missing.

TRANSACTIONS ARE CATEGORIZED INCORRECTLY

This is a common accounting error. For instance, a company hires some extra temporary labor for a busy period in their factory. The accounting department later catalogs those labor payments under “operating expenses” instead of under “inventory costs” (which is where factory labor costs should go). If the labor costs are still debited and credited fully, then this type of mistake can also be difficult to catch. However, it will most likely be caught if there’s an audit.

TIME CONSUMING AND COSTLY

A double entry system is time-consuming for a company to implement and maintain, and may require additional manpower for data entry (meaning, more money spent on staff). This will depend on the amount of business a company does.

Even with the disadvantages listed above, a double entry system of accounting is necessary for most businesses. This is because the types of financial documents both businesses and governments require cannot be created without the details that a double entry system provides. These documents will allow for financial comparisons to previous years, help a company to better manage its expenses, and allow it to strategize for the future.

Why Can’t Single Entry Systems Use T Accounts?

A single entry system of accounting does not provide enough information to be represented by the visual structure a T account offers. A single entry system records each of a company’s financial transactions as a single entry in a log, as opposed to a double entry system which assigns each transaction to a category and records both a debit and credit for each.

T Accounts allows businesses that use double entry to distinguish easily between those debits and credits.

RELATED ARTICLES

What Are Provisions in Accounting?

What Are Provisions in Accounting? Is Inventory a Current Asset?

Is Inventory a Current Asset? Operating Expenses (OpEx): Definition, Formula, and Example

Operating Expenses (OpEx): Definition, Formula, and Example What is the Difference Between Financial and Managerial Accounting?

What is the Difference Between Financial and Managerial Accounting? What is the Direct Write Off Method?

What is the Direct Write Off Method? How to Calculate Depreciation

How to Calculate Depreciation