Capital Loss Carryover: Definition & Meaning

There are many things to know when it comes to taxes for your business. Every business except a partnership must file income taxes each year. But you also need to consider estimated taxes, sales taxes, employment taxes, and more.

And what about capital gains and losses? What can be done about these? There are certain circumstances, but a capital loss carryover is something else to keep an eye on. Read on to learn all about it.

![]() Table of Contents

Table of Contents

KEY TAKEAWAYS

- Up to $3,000 in ordinary taxable income can be deducted from capital losses over capital gains in a single tax year.

- Net capital losses in excess of $3,000 may be carried forward until the carrying capacity is reached.

- Investors must be careful not to repurchase any stock sold for a loss within 30 days due to the wash-sale IRS regulation, or the capital loss will not be eligible for favorable tax treatment.

What Is Capital Loss Carryover?

Capital loss carryover is the entire amount of capital losses that may be carried over to a later tax year. There is a $3,000 annual cap on the number of net capital losses that can be deducted from income. Net capital losses are the difference between total capital losses and total capital gains.

Net capital losses above the $3,000 cap may be carried forward to subsequent tax years up to their full amount. The number of years that a capital loss may be carried over is unlimited.

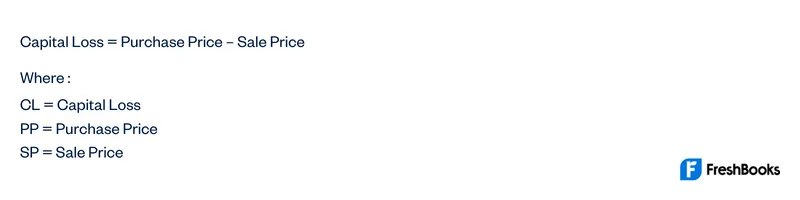

How Is Capital Loss Calculated?

The following is the formula for capital loss:

A capital gain is defined as when the sale price exceeds the buying price.

How Does Capital Loss Carryover Work?

Investment losses have a less severe impact because of capital loss tax allowances. However, the provisions do not come without exceptions. Wash sale laws, which forbid repurchasing an investment within 30 days of selling it for a loss, should be taken into consideration by investors.

If this happens, the capital loss is added to the cost basis of the new position rather than being used in tax computations, which lessens the impact of future capital gains.

How to Claim a Capital Loss

You must submit IRS Form 8949, “Sales and Other Dispositions of Capital Assets,” along with your tax return in order to claim capital losses. Along with your Form 1040, you must include Schedule D, “Capital Gains and Losses.”

The purpose of Form 8949 is to help the IRS compare the data provided by brokerage and investment businesses with the data you included on your tax return.

Example of Carrying Over Capital Losses

Extra capital losses may be applied to future returns and taxable income. Let’s say that Company X has an unrealized loss of $40,000; the investor might roll the difference over to subsequent tax years.

The investor would pay no capital gains tax for the whole year because the initial $10,000 of realized capital gain would be a capital gain offset. Additionally, $3,000 may be deducted from ordinary income in the same tax year.

The investor would have $27,000 in capital losses to roll over to subsequent years once the $10,000 capital gain and the $3,000 ordinary income were offset. Losses may be carried over into future tax years without being limited to the current tax year.

Summary

A corporation has a capital loss when the value of its investments, capital assets, and other assets decreases. When capital assets are sold for less than they were originally worth, a loss is incurred.

Loss of capital is tax deductible. It implies that capital losses may be taken into consideration in order to lower the overall amount of taxable income.

FAQS on Capital Loss Carryover

You are permitted to carry forward a net capital loss indefinitely. Regular monitoring of the capital loss carryover amount will be simpler if the investor accurately documents all of that data.

Your net loss is restricted by the IRS to $3,000 for single filers and married couples filing jointly for married people filing separately, $1,500.

You can deduct some income from your tax return by using capital losses to offset capital gains within a taxable year.

Sadly, the IRS does not permit the investor to select the year in which they will apply the carryover loss. If the investor misses a year without making up the loss, the forfeit is irrevocable.

You can anticipate receiving a notice from the IRS classifying the full amount as a short-term gain and attaching a bill for taxes, penalties, and interest if you fail to report it.

Share: