Average Cost Method Definition & Examples

The average cost method is a way of calculating the cost per item that has been sold. This method takes the total cost of all individual units in stock and divides it by the number of items that have been sold. The average cost method is used by businesses to help them understand their profits and losses on individual items that have been sold.

This article will discuss the average cost method in detail. Topics will include what it is, examples of the method, and more.

![]() Table of Contents

Table of Contents

KEY TAKEAWAYS

- There are a few different inventory methods that businesses can use when calculating the cost per inventory unit.

- An average cost method is a good option for small businesses that have a variety of products with different costs of units.

- Watch out for common inventory obstacles like Inventory damage, Scalability, and understocking or overstocking.

- Consult a tax professional if you’re unsure about which method to use.

What is the Average Cost Method?

The average costing method is a way of calculating the cost of items sold. This method is used by businesses to help them understand their profits and losses on individual items.

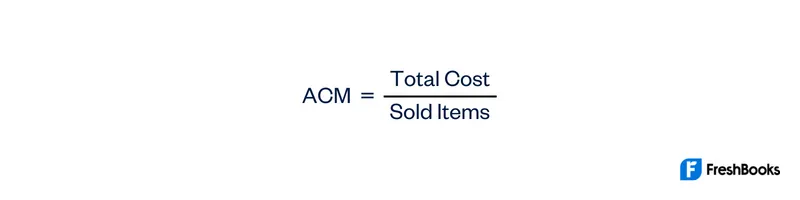

Calculating the Average Cost

ACM is the total cost of all items in stock divided by the number of items that have been sold. This calculation gives you the average cost per unit for the items that have been sold.

Example of the Average Cost Method

Let’s say that a business has inventory that costs $1,000 and they have sold 100 items. Their ACM would be $10 per item. This means that the average cost of each item that was sold was $10.

What is Weighted Average Cost?

Some businesses use weighted average cost in addition to ACM. This calculation takes the cost of each item and multiplies it by the number of items that have been sold. The sum of these calculations gives you the weighted average cost.

Why is Weight Average cost used?

The weighted average cost is used when the cost adjustment of an individual item changes over time. It’s also used when certain products sell much more often than others. This calculation gives you a more accurate representation of the cost per unit for the items that have been sold.

Benefits of the Average Cost Method

The average cost method has a few benefits that businesses should consider.

- It’s an easy calculation to make. This can be a quick analysis for any business.

- This method is unbiased. This means that it doesn’t favor one product over another.

- Weight ACM gives a more accurate view of the cost of inventory sold. This is because weighted average cost takes into account the number of items that have been sold.

Disadvantages of ACM

Here are a few disadvantages of using average cost.

- It does not take into account the age of the inventory. This can be important for businesses that want to sell or get rid of older inventory.

- It groups all different kinds of products together. This can make it difficult to understand the profits and losses for specific items.

- It’s easily skewed. This calculation can be thrown off by a few high-cost items.

Businesses should consider the pros and cons of using average cost when making decisions about their inventory. This calculation can help businesses better understand their profits and losses on individual products.

What Kind of Companies Use Average Cost Method?

Any company that sells products can use the average cost method. This calculation is especially helpful for businesses that have a variety of different product costs. This method can also be used when a company has seasonal fluctuations in their sales.

Here are some of the most popular industries using the Average Cost Method:

- Food and beverage

- Clothing and accessories

- Department stores

- Hardware and home improvement

- Auto parts

- Pharmaceuticals

What is the Difference Between Average Cost and Standard Cost?

There are a few main differences between average cost and standard cost. One is that average cost takes the total cost of all items in stock. Then, you divide it by the number of items that have been sold.

Standard cost is not a moving average like average cost. It provides separate inventory valuation methods for the cost of each item.

Which Method is Better for Companies?

There is no right or wrong answer when it comes to which method a company should use. It depends on the individual business and their specific needs.

- The average cost method is a more simplified approach. This can be helpful for businesses that have a lot of inventory and sell a variety of products.

- Weighted average cost is better for businesses that have products with different costs and those that experience fluctuations in their sales.

- Standard cost is beneficial for businesses that want to track the cost of each individual product.

Are There Other Inventory Accounting Methods?

Yes, there are a few other common methods that businesses can use when calculating the cost of their inventory.

1: First In, First Out (FIFO)

This is when you track the items that were bought first and sold first. This method assumes that the old items are always sold first.

2: Last In, First Out (LIFO)

This is the opposite of FIFO. LIFO assumes that the new items are always sold first.

3: Specific Identification Method

The specific identification method of inventory attaches the actual cost to a specific product. This method is effective when purchasing and selling large inventory items like machinery or cars.

Which Inventory Method is Best for Small Businesses?

Again, there is no right or wrong answer when it comes to which inventory method is best. It depends on their individual needs and what products they are selling.

The average cost method is a good option for small businesses that have a variety of products with different aggregate costs. This calculation is simple and easy to understand for a smaller team.

Common Inventory Obstacles You May Encounter

Now that you understand the basics of average cost, there are a few things you should be aware of related to inventory.

1: Inventory is damaged or obsolete

This can distort your calculations and throw your results off. It’s important to note that this inventory is not sold and should be excluded from your average cost.

A solution for this is to create a reserve for damaged or obsolete inventory. This will help you account for these costs in your calculation.

2: Scalability

Manually tracking inventory is reasonable during the early stages of a business. However, as the business grows, it becomes increasingly difficult to manage. In addition, if you grow into multiple warehouses or manufacturers, it can become more difficult still.

A solution for this is to invest in inventory software that can automate the process. This will help you save time and ensure an accurate calculation of your average cost estimates.

3: Overstocking or Understocking

If you have too much inventory, it can be costly to maintain. This is because you are paying for the product even if it is not sold. On the other hand, if you do not have enough inventory, you may not be able to meet customer demand. This can lead to missed sales and lost sales revenue. It can take time to find the sweet spot for your inventory.

A solution for this is to regularly evaluate your stock levels and make changes as needed. This will help you maintain an accurate average cost of inventory items.

Summary

This guide has the basics of the average cost method. It also highlighted some common inventory obstacles that small business owners can encounter. Finally, we shared our advice for choosing which inventory accounting method is best for your small business based on your specific needs.

FAQs on Average Cost Method

Different methods can result in substantially different amounts of net profit. If you’re unsure, consult a tax professional.

Simply add up the total individual cost of all items and divide by the number of items that have been sold.

Yes, the average cost method is perfect for businesses that sell a variety of products.

The Weighted-average method takes into account the number of items that have been sold. This makes it more accurate than ACM.

Share: