EBITDA Definition, Formula, Calculation & Example

When you’re running a business, earnings tend to be a hot topic of discussion. Often, earnings get brought up when discussing the operating performance of a business. Still, more often, the acronym EBITDA comes up regularly.

Are you familiar with EBITDA? If not, as a business owner, you should be. In this article, we’re going to cover exactly what EBITDA is and how you can use it to determine the success of your business.

![]() Table of Contents

Table of Contents

KEY TAKEAWAYS

- While EBITDA isn’t the most useful financial metric for reporting, it is an effective tool that works well as an earnings metric.

- EBITDA removes the specific expenses of a business and allows it to compare itself to others. This puts businesses on a mostly level playing field, which makes comparisons much easier.

What Is EBITDA?

EBITDA is an acronym that stands for: “Earnings Before Interest, Taxes, Depreciation, and Amortization.” In many instances, EBITDA serves as a measure of profits and financial performance for a business. It is sometimes a good replacement for net income.

Breaking EBITDA Down

Now, to truly understand EBITDA, you have to break it down entirely. Thankfully, the acronym makes this pretty easy. Let’s take a look:

- Earnings: Money earned by the company

- Before: This one is self-explanatory

- Taxes: The money paid to the government by a company based on its tax rate

- Depreciation: Decreases in the value of a company’s capital assets

- Amortization: The cost of an intangible asset, spread out over time

EBITDA is a Heavily Used Comparison Tool

When it comes to comparing businesses in a specific industry, many financial experts use EBITDA. It’s a commonly used profitability metric that allows financial experts to determine profitability among companies.

Using EBITDA has become common for measuring core profit trends. Why? Because of the way it eliminates extraneous factors. It’s also useful for finding more accurate comparisons between companies in similar industries.

Additionally, EBITDA works well as a starting point to estimate cash flow. This allows business owners and experts to determine a company’s ability to pay off long-term debts.

EBITDA is Not a Required Reporting Measure

Companies are not required to report EBITDA at this time. It can be easily found in a company’s income statement. The income statement reports a company’s revenue and operational expenses for a set period of time.

The EBITDA Formula(s)

Let’s use each formula and see how it’s used to calculate EBITDA.

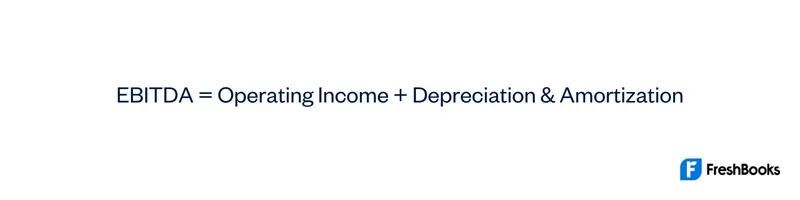

Formula 1: Operating Income

If you’re calculating EBITDA and you have a company’s operating income, the formula is straightforward.

You can find operating income by reviewing an income statement or a balance sheet. Either financial statement has the information you need.

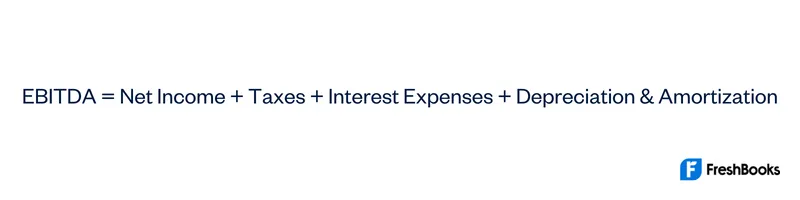

Formula 2: Net Income

The second EBITDA formula uses net income, as well as a few other variables. Overall, the information is the same, though. The idea is that when you add net income, taxes, and interest expenses, you’ll find the operating income. For example:

This formula is more suited for using a company’s income statement. The income statement itself will normally have these figures as their own line items.

An Example of EBITDA

Now that we know both of the formulas, let’s look at an example of calculating EBITDA. For the purpose of this example, let’s say we are looking at a company’s income statement, which shows the following figures:

- Net Income = $400,000

- Taxes = $200,000

- Interest Expenses = $150,000

- Depreciation & Amortization = $110,000

Now, let’s plug these figures into the EBITDA formula:

EBITDA = $400,000 + $200,000 + $150,000 + $110,000

EBITDA = $860,000

It’s as simple as that. EBITDA is a simple calculation that just about anyone can do to see whether they have a healthy company. It’s how you use it that really counts.

Understanding EBITDA More Clearly

In the simplest definition, EBITDA is really just net income with certain expenses added back. These include taxes, interest, depreciation, and amortization. By removing the variables mentioned above, you can see how well a business is doing. Once you remove these expenses from the picture, all you have left are true operating expense figures.

How Companies Use EBITDA to Their Advantage

While EBITDA isn’t a required financial metric, many companies still pivot to it at times. In general, a company will focus on its EBITDA if its net income is down. This is because EBITDA tends to be an inflated number, regardless of actual income.

It’s important to note that EBITDA negates a company’s amortization expense and depreciation expense. In the early lives of companies, there can be higher depreciation and amortization due to the company investing in capital assets that have depreciated.

Weaknesses in EBITDA

While EBITDA is a great financial metric, it isn’t all good. Like any other selective reporting, it’s important to explain some weaknesses of EBITDA. We’ve touched on the fact that you can use it to hide poor financial performance, but there are other things to consider too.

EBITDA Does Not Fall Under GAAP

EBITDA is a non-GAAP metric. This means that it doesn’t fall under the Generally Accepted Accounting Principles (GAAP). This can mean that a company can calculate EBITDA in various ways, but at the end of the day, companies that follow GAAP still need to ensure that their income statement is in accordance with the rules. Since EBITDA is calculated using operating income or net income from the company’s income statement, this doesn’t necessarily pose a large risk.

EBITDA Ignores the Cost of Assets

One primary concern of EBITDA is that it ignores the cost of assets. When you remove how much a loan costs, or the depreciation of an asset, you remove how much it’s worth to the company.

Comparing EBITDA to Other Statements

Because EBITDA is a skewed metric of sorts and not a GAAP metric, it’s important to know other statements that may be more useful. EBITDA is often compared to the following:

- EBIT or EBT tend to be a more accurate way of measuring business performance. You can derive these from EBITDA, but they only add back expenses that are outside of a company’s control. As such, many experts see them from a more honest perspective.

- Balance sheets allow analysis of a company’s assets and liabilities. This allows a company to review the company’s liquidity or ability to pay debts and how much of the assets are offset by debt and equity.

- Cash Flow Statement is a better metric for looking at how much cash a company is generating. This is because it adds non-cash charges back to net income and includes changes in working capital.

If a company is relying solely on EBITDA, it may be better off using the above options in addition to EBITDA. These give interested parties a better idea about a company’s financial performance.

Summary

Companies that use EBITDA generally do so to evaluate the profitability of a business. The metric includes both earnings and operating expenses. As such, it gives a more complete picture of a company’s earnings potential than other financial metrics. Additionally, because EBITDA works so well for evaluation purposes, it’s a great way to partly measure the health of a company. However, EBITDA is only one part of reviewing a company’s financial health.

Frequently Asked Questions

EBITDA is a way of looking at the cash earnings of a company and its potential future growth. It removes specific expenses that a company is paying and shows just how much money it is generating.

No, gross profit is the profit left over after production costs get subtracted and before operating costs and overhead. We know that EBITDA is also a measure of profitability of earnings before removing interest, taxes, depreciation, and amortization.

Not only is it a great way to measure profitability trends, it’s also ideal for providing accurate comparisons of businesses. Moreover, EBITDA works well as a starting point for estimating cash flow availability for long-term debt payments.

A higher EBITDA is preferable, as it reflects lower production costs and operating expenses. When these expenses are lower, it results in greater profitability.

Income taxes are added back to operating income and payroll taxes would be included in wages and benefits line of operation expenses. Additionally, local, federal, and state corporate taxes.

Share: