How To Prepare An Income Statement

To prepare an income statement, small businesses must analyze and report their revenues, operating expenses, and the resulting gross profit or losses for a specific reporting period. The income statement, also called a profit and loss statement, is one of the major financial statements issued by businesses, along with the balance sheet and cash flow statement.

If you have found yourself struggling to find the time to create your own profit and loss report, or P&L, from scratch, a free invoice statement template is the perfect solution.

FreshBooks provides free template income statements that are pre-formatted for your needs. All you need to do is fill in the empty fields with the numbers you’ve calculated. No stress, just results.

Key Takeaways

- Profit and loss documents are one of the key financial statements a company uses

- You can choose to report annually, quarterly, or on a monthly basis

- Publicly traded companies must prepare financial statements quarterly and annually

- Your revenue includes all the money earned for your services during the period

- Include all of your business operating expenses to get an accurate financial landscape

- Profit and loss statements provide a future understanding for the coming fiscal period

These topics will show you how to prepare an income statement:

- What Is An Income Statement?

- Steps to Prepare an Income Statement

- Importance and Uses of an Income Statement

- Income Statement Example

- What’s the Difference Between a Balance Sheet and Income Statement?

- Conclusion

- Frequently Asked Questions

What Is An Income Statement?

Income statements or profit and loss accounts are financial statements used to calculate the financial health of the company.

It shows the company’s revenues and expenses during a particular period, which can be selected according to the company’s needs. A P&L, which stands for profit and loss, indicates how the revenues are transformed into net profit. There are two ways of preparing P&L single step and multi step income statement. Single step gives you the revenue, expenses and the profit or loss of the business while Multi step breaks down operating revenues and operating expenses versus non-operating revenues and non-operating expenses.

A quarterly income statement shows the gross profit or loss generated by your business over a three-month period. It can also be referred to as a profit or loss account and is a crucial financial statement that shows the business’s operating income and expenditures, detailing your net income or net profits.

Steps to Prepare an Income Statement

Below is a 10-step guide on how to write a professional income statement. Using this process, along with the FreshBooks income statement template, allows you to simply fill in the details rather than spending time creating an entire document from scratch.

1. Pick a Reporting Period

The first step in preparing an income statement is to choose the reporting period your report will cover. Businesses typically choose to report their P&L on an annual, quarterly, or monthly basis. Publicly traded companies are required to prepare financial statements on a quarterly and yearly basis, but small businesses aren’t as heavily regulated in their reporting.

Creating monthly income statements can help you identify trends in your gross profit and expenditures over time. That information can help you make business decisions to make your company more efficient and profitable.

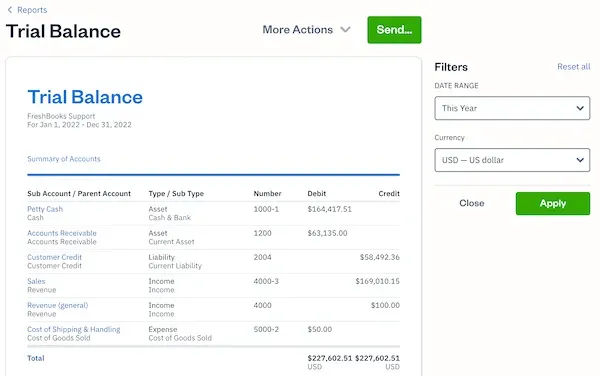

2. Generate a Trial Balance Report

To create an income statement for your business, you’ll need to print out a standard trial balance report. You can quickly generate the trial balance through your cloud-based accounting software. Trial balance reports are internal documents that list the end balance of each account in the general ledger for a specific reporting period.

Creating balance sheets is a crucial part of creating a profit and loss, as it’s how a company gathers data for its account balances. It will give you all the end balance figures you need to create an income statement.

3. Calculate Your Revenue

Next, you’ll need to calculate your business’s total sales revenue for the reporting period. Your revenue includes all the money earned for your services during the reporting period, even if you haven’t yet received all the payments. Add up all the revenue line items from your trial balance report and enter the total amount in the revenue line item of your P&L.

FreshBooks accounting software provides an easy-to-follow accounting formula to make sure that you’re calculating the right amounts and creating an accurate income statement.

4. Determine the Cost of Goods Sold

Your cost of goods sold includes the direct labor, materials, and overhead operating expenses you’ve incurred to provide your goods or services. Add up all the cost of goods sold line items on your trial balance report and list the total cost of goods sold on the statement directly below the revenue line item.

5. Calculate the Gross Margin

Subtract the cost of goods sold total from the revenue total on your income statement. This calculation will give you the gross margin, or the gross amount earned from the sale of your goods and services.

6. Include Operating Expenses

Add up all the operating expenses listed on your trial balance report. Each expense line should be double-checked to make sure you have the correct figures. Enter the total amount into the statement as the selling and administrative operating expenses line item. It’s located directly below the gross margin line.

7. Calculate Your Income

Subtract the selling and administrative expenses total from the gross margin. Doing this will give you the amount of pre-tax operating income. Enter the amount at the bottom of the income statement.

8. Include Income Taxes

To calculate income tax, multiply your applicable state tax rate by your pre-tax income figure. Add this to the statement below the pre-tax income figure.

9. Calculate Net Income

To determine your business’s net income, subtract the income tax from the pre-tax income figure. Enter the figure net income into the final line item of your income statement. This will give you a general understanding of your business performance, letting you see how profitable you have been.

10. Finalize the Income Statement

To finalize your statement, add a header to the report identifying it as an income statement. Add your business details and the reporting period covered by the profit and loss. With all of the data you’ve compiled, you’ve now created an accurate statement.

This statement will give you a future understanding of your company’s fiscal health that will be of great benefit to you and your business practice.

Don’t let income statements monopolize your time. FreshBooks offers a wide variety of accounting services that save you time and money when creating financial statements. Learn more about FreshBooks accounting software and give them a try for free.

Importance and Uses of an Income Statement

Income statements help business owners discover if they can generate profit by increasing revenues, decreasing costs, or a combination of both. They also show the outcome of strategies a business sets at the beginning of a fiscal period, allowing them to make impactful adjustments to maximize profit.

By using income statements, management can make informed decisions. A detailed income statement can lead to expansion, pushing sales, increasing production capacity, streamlining the sale of assets, or shutting down a specific department, project, or product line. Companies can also use competitors’ income statements to gain insights into the success of a company and how they focus their time and resources in various focus areas.

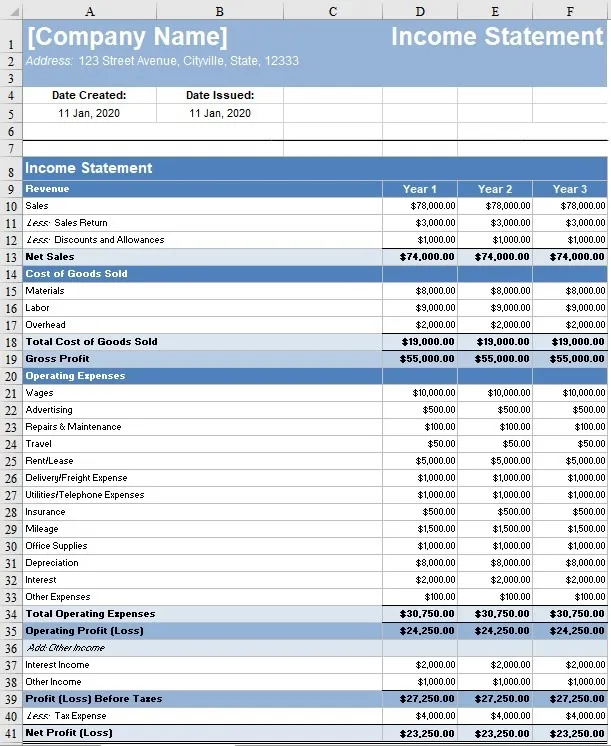

Income Statement Example

This is an example of an income statement created by FreshBooks. It can give you a better understanding of what’s reported on a statement, the format, and how the data should be laid out:

What’s the Difference Between a Balance Sheet and Income Statement?

There are a few key differences between the balance sheet and the statement, including:

- Timing: While the profit and loss document reports financial activity for a specific reporting period, usually a month, a quarter, or a year, the balance sheet reports financial activity at a specific point in time for a snapshot view of a business’s finances.

- Information reported: The statement reports on a business’s revenues and expenses and, ultimately, the amount of gross profit or loss generated, whereas a balance sheet reports on a company’s assets, liabilities, and equity.

Keep track of your business finances easily and efficiently. FreshBooks offers bookkeeping services that take the guesswork out of your accounting. Learn more about how FreshBooks bookkeeping services can support your accounting needs.

Conclusion

Whether you’re an individual contributor, a leadership team member, or an entrepreneur wearing many hats, knowing how to write an income statement provides a deeper understanding of the financial state of your business. It can also help improve financial analysis, allowing you to plan for the future and scale your business successfully. If you want to learn the correct way of creating and analyzing an income statement, you can follow our guide on financial statement examples, where we have explained each point in detail to give you a better understanding.

Frequently Asked Questions

What are the most important figures in an income statement?

The most important figures in your statement include your gross margin, operating earnings, and pretax earnings. These figures are critical for the equity and credit analysis processes that will benefit the future growth of your business.

What is not included in an income statement?

Income statements don’t differentiate cash and non-cash receipts or cash vs. non-cash payments and disbursements. EBITDA (earnings before interest, taxes, depreciation, and amortization) can be included but are not present on all P&Ls.

Is profit and loss the same as an income statement?

Yes. There is no difference between an income statement and a profit and loss report. The terms can be used interchangeably.

How do I know if my income statement is correct?

Avoiding common accounting errors is the best way to ensure the accuracy of your income statement. Keeping an audit trail, double-checking your work, having a consistent process, conducting routine reconciliations, and allowing a fresh set of eyes to review your work are the best ways to keep information on your income statement correct.

Should the balance sheet and income statement match?

No. You will not get your balance sheet and income statement to match. These two reports feature different line items, meaning the end number and the data being gathered are not identical.

Do you put negative in the income statement?

Yes. A negative income figure appears on a company’s income statement. A negative net income means a company has a loss over that given account period, not a profit. While your business may have positive sales, you’ll end up with a negative net income if expenses and other costs exceed that amount.

About the author

Jason Ding is a seasoned accountant with over 15 years of progressive experience in senior finance and accounting across multiple industries. Jason holds a BBA from Simon Fraser University and is a designated CPA. Jason’s firm, Notion CPA, is an accounting firm with a business-first focus. The firm specializes in preparing personal and corporate taxation while providing fractional CFO work and leading the accounting and finance function for several small-to-medium-sized businesses. In his free time, you’ll find Jason on the basketball court, travelling, and spending quality time with family.

RELATED ARTICLES

Single-Entry Bookkeeping: Single-Entry vs Double-Entry

Single-Entry Bookkeeping: Single-Entry vs Double-Entry What Are the Different Types of Accounting Systems? Options Explained

What Are the Different Types of Accounting Systems? Options Explained How to Be Your Own Accountant in 7 Steps

How to Be Your Own Accountant in 7 Steps CPA vs Accountant: What Is the Difference?

CPA vs Accountant: What Is the Difference? How Much Do Accountants Charge for a Small Business? It Depends on Your Needs

How Much Do Accountants Charge for a Small Business? It Depends on Your Needs