What is Opening Balance Equity and How to Fix It?

An opening equity balance account is usually created automatically. It is only meant to be a temporary account. Not closing out this account makes your balance sheet look unprofessional and can also indicate an incorrect journal entry in your books.

If you have been asking yourself, “What is opening balance equity on a balance sheet?” you will find your answer in this guide. We will go over opening balance equity, the reasons it’s created, and how to close it out so your balance sheets are presentable to banks, auditors, and potential investors.

Key Takeaways

- While opening equity balance accounts are not something to worry about, they should be closed out promptly to avoid confusion and unbalanced financial reports

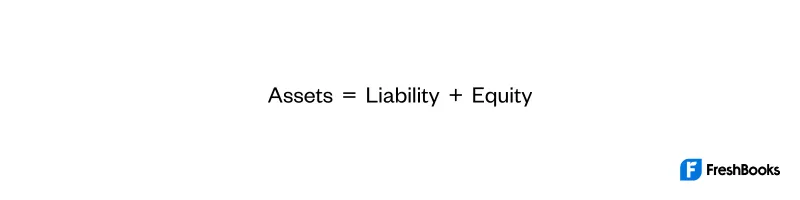

- A balance sheet should equal out to zero at the end of each reporting period, using the equation Assets = Liability + Equity

- EBAs are created automatically by accounting software for several reasons, including a first entry into new software, the initial addition of a bank or credit card account, a new inventory item, or a new vendor or customer being added

- If your company is a corporation, you may close out balance equity to a retained earnings account

- If your company is a sole proprietorship, you may close out the balance equity to an owner’s equity account

Here’s What We’ll Cover:

What Is Opening Balance Equity?

Balance Sheet 101: Understand Opening Balance Equity Accounts

Reasons for Opening Balance Equity

Bringing an Opening Balance Equity Account to Zero

Managing Opening Balance Equity for Presentable Balance Sheets

Opening Balance Equity vs. Retained Earnings

Importance of Accurate Opening Balance Equity

What Is Opening Balance Equity?

Opening balance equity is an account created by accounting software to offset opening balance transactions.

Opening Balance Equity accounts show up under the equity section of a balance sheet along with the other equity accounts like retained earnings but may not show up on the opening balance sheet if the balance is zero. This is good because opening balance equity should be temporary by design.

FreshBooks accounting software offers various features that help manage opening balance equity effortlessly. Sign up or try it now for free.

Balance Sheet 101: Understand Opening Balance Equity Accounts

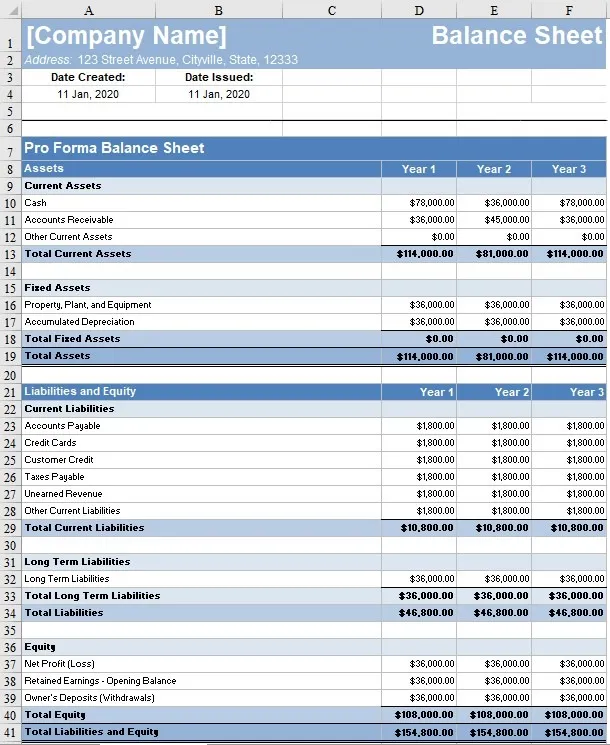

Three categories make up a balance sheet: Assets, liabilities, and equity.

The fundamental balance sheet equation is:

Balance sheet account transactions should cancel out at zero. So if you post a new asset account with a balance, you’d need to offset it by the same amount on the other side of the equation when you first bring balances into accounting software. Using accounting software can help you figure out what is missing, or you can fill out an accounting template and see the numbers in front of you. Click here for free downloadable templates you can use now.

Here’s an opening balance equity example for a clearer explanation: Suppose an asset account like a checking account with a $100 balance gets added to accounting software. The opening balance equity account has to be credited $100 so the balance sheet balances. In this context, the balance of the open balance equity account would then temporarily be $100 to match the opening balance of the bank account.

Reasons for Opening Balance Equity

The software creates an opening balance equity account for several reasons, including:

- Creating a data file for new businesses with beginning balances

- Initial addition of bank and credit cards with account balances

- The first entry into a new accounting software

- Adding a new item to the chart of accounts, such as a new inventory

- New vendor or customer entry with value balances (for example, outstanding balances which result in an accounts receivable opening balance)

Sign up for accounting software to easily create and manage your opening balance equity account here.

Common Errors to Avoid

Opening balance equity should be temporary. However, it’s common to carry a balance for a considerable period.

A common reason for a lingering balance on your opening balance equity account includes bank reconciliation adjustments that weren’t done properly. Always make sure to account for uncleared bank checks and other factors.

If the journal accounting entry amount doesn’t match your bank account statement and you close it out, then the software will adjust the opening balance equity account balance. For a free trial of accounting software, click here.

Other reasons include:

- Not knowing it is an undesirable state for your balance sheet to be in

- A transaction is mislabeled to the opening balance equity account

- An opening balance equity account wasn’t deactivated

Bringing an Opening Balance Equity Account to Zero

Make your balance sheet look more professional and clean by clearing the balance in this account and bringing it to zero.

You or your bookkeeper can make journal entries to close this account in various ways. Here’s the most common method:

- If your company is a corporation: Close out the balance equity to “Retained Earnings.”

- If your company is a sole proprietorship: Close out the balance equity to “Owner’s Equity.”

If it’s a positive balance, put a debit entry to the opening balance equity account and a credit to the owner’s equity account (or retained earnings account.)

If it’s a negative balance, put a credit entry to the opening balance equity account and a debit to the owner’s equity account (or retained earnings account.)

Keep in mind that closing the balance equity to retained earnings or owner’s equity is essentially the same concept. These equity accounts are just labeled differently to represent the ownership or form of a business.

Note: Consult your CPA before touching the retained earnings account.

Managing Opening Balance Equity for Presentable Balance Sheets

Opening balance equity should only be temporary. Having a balance on your opening balance equity account makes your balance sheet look unprofessional.

The best practice is to close opening balance equity accounts off to retained earnings or owner’s equity accounts. A professional bookkeeper will help you ensure your books are up-to-date and accurate. Click here for a free trial of the FreshBooks bookkeeping and accounting services now.

Opening Balance Equity vs. Retained Earnings

Opening balance equity is an account created by accounting software in an attempt to balance out unbalanced transactions that have been entered. The software generates this number to show an accounting error or unbalanced debit or credit on the balance sheet.

The difference between opening balance equity and retained earnings is that retained earnings are a type of equity, meaning they are the profit a company still has left after paying off debts, costs, taxes, and shareholder dividends. This is also known as net profits or net earnings of a company, and as a form of equity, it can be reinvested into the company for growth purposes and is used to determine what the business is worth.

Importance of Accurate Opening Balance Equity

- Impact on financial statements

An OBE account may cause confusion with financial statements, showing a temporary number that looks unprofessional and an unbalanced journal entry that needs to be reconciled.

- Effect on the company’s decision-making process

Not having an accurate financial picture of where all the money is coming from may affect whether you make big financial moves.

- Importance for tax purposes

Ensuring all finances are accounted for will make filing your income taxes much easier. Maintain professional balance sheets and simplify accounting reports with FreshBooks.

Conclusion

If you find yourself with an opening balance equity account at the first of the month, don’t panic. It is simply an automated function programmed into accounting software demonstrating an issue with the previous term’s balance sheet. There are many reasons why an EBA would show up, but if you have not made any new bank or client additions lately, they may be due to missing uncleared bank checks or a journal accounting entry amount that does not match your bank statement.

Although not a huge issue, it is important to close it out right away, as it can confuse and mislead others about your finances.

FAQs on Opening Balance Equity

Is opening balance equity a positive or negative?

It is negative in that it can affect your current month’s finances.

An opening balance equity can be in a positive-sum or a negative number. If it is a positive balance, you will need to put a credit entry into the opening balance equity’s account and then add a debit to the owner’s retained earnings or equity account, and if it is negative, add a debit toward the opening balance equity account and credit the owner’s retained earnings or equity account.

What is the difference between opening balance equity and owner’s equity?

Opening balance equity is the closing balance of the last reporting period that automatically shows up in accounting software as a new account. This number is generated when there are unbalanced transactions in the previous term’s balance sheet.

Owner’s equity is the proportion of company assets that the business owners can claim. It is calculated by taking the amount of money the owner of a business has invested and subtracting all liabilities and debt.

Should opening balance equity be zero?

Ideally, yes, your opening balance equity should be at zero. If it is not, this means an unbalanced or unaccounted-for entry in your balance sheet needs to be looked at closer.

How do you calculate the opening balance?

You will enter the amount of money your business starts with at the beginning of your reporting period (usually the 1st of each month). Your opening balance will be the closing balance of the last reporting period, ideally, zero, with all accounts balanced.

How do I get rid of opening balance equity?

It is not difficult to get rid of the opening balance equity account, all you need to do is make an adjusting entry that transfers the balance amount into the business owner’s retained earnings account or their capital account.

More Resources on Small Business Accounting

About the author

Jami Gong is a Chartered Professional Account and Financial System Consultant. She holds a Masters Degree in Professional Accounting from the University of New South Wales. Her areas of expertise include accounting system and enterprise resource planning implementations, as well as accounting business process improvement and workflow design. Jami has collaborated with clients large and small in the technology, financial, and post-secondary fields.

RELATED ARTICLES

Unlevered Free Cash Flow (UFCF): Guide, Formula & Examples

Unlevered Free Cash Flow (UFCF): Guide, Formula & Examples How to Become a Bookkeeper: A Step By Step Guide

How to Become a Bookkeeper: A Step By Step Guide What is a Pay Stub? Examples for Businesses

What is a Pay Stub? Examples for Businesses What is Operating Cash Flow Formula? (OCF Formula)

What is Operating Cash Flow Formula? (OCF Formula) What Is Net Pay and How To Calculate It

What Is Net Pay and How To Calculate It What Is Gross Pay and How To Calculate It

What Is Gross Pay and How To Calculate It