Accounting for Entrepreneurs: A Guide for Small Business

As an entrepreneur, you can set your business up for financial success by mastering the basics of small business accounting. Proper accounting can help you understand the financial health of your company, plan for future growth and ease the burden of tax season.

Key Takeaways

- Understanding accounting can help entrepreneurs grow their small businesses.

- Choosing the right business structure and accounting system is key to growing your business.

- Monitoring your accounting can empower entrepreneurs to develop effective business strategies.

- The right automation software makes it easier to manage your own bookkeeping and accounting.

Table of Contents

- 8 Basics of Accounting for Entrepreneurs

- What are the Benefits of Accounting for Entrepreneurs?

- Enhance Your Accounting with FreshBooks

- Frequently Asked Questions

8 Basics of Accounting for Entrepreneurs

Adopting proper accounting practices when you launch your business is crucial to succeeding as an entrepreneur. You don’t need to be an accounting expert to oversee your business finances, you just need to follow these basic accounting steps for entrepreneurs:

1. Register Your Business

The first step in getting a handle on your finances as an entrepreneur is to register your business. You’ll also need to make sure you have all the necessary business licenses, which vary by industry and state. This business license guide can help you find out what you need. You can choose from a few different business models to register your business, including:

- Sole Proprietorship: An unincorporated company with only one owner, sole proprietorships are a good option for entrepreneurs because the registration process is easy and affordable. As a sole proprietorship, there’s no separation between you and your business, so you can file your business taxes as part of your personal income tax return. A potential downside, however, is that you can be held personally liable for business debts.

- Limited Liability Company: A LLC combines features of a sole proprietorship and a corporation, where you’re protected in the case of company debts, but you have flexibility with filing your taxes either through your personal income tax or a separate business filing.

- Partnership: If you have a business partner and want to share ownership of the company, this is a good option. Each partner is required to bring something to the business, whether it’s skills, money or property. You’ll want to have a formal partnership agreement in place to outline your roles and expectations.

- Corporation: Corporations are the most complex business structure and they’re expensive and time consuming to set up. A corporation is a company that is legally allowed to act as a single entity and is considered a single taxpayer. Some of the benefits of launching a corporation include lower tax rates and greater legal protections.

2. Open a Business Bank Account

Entrepreneurs need to separate their personal and business finances. If you don’t keep your finances separate, you can easily lose track of business expenses, complicate your accounting system and you could even run into legal trouble. The easiest way to keep your business finances apart is to open a business bank account. A business checking account may be all you need when you’re starting out as an entrepreneur, or you may also want to get a savings account. Before choosing a bank for your business, make sure it meets all your needs:

- Compare the small business banking fees offered by different banks

- Make sure there are ATMs near your office or home for convenience

- Look into the transaction limits of different banking options and make sure they work for your business

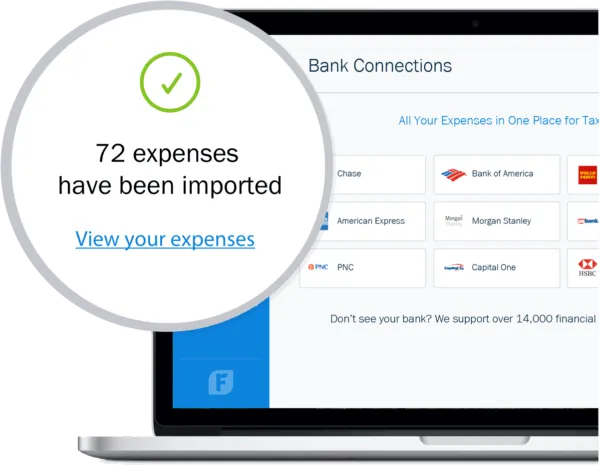

Having a business bank account also makes it easier to track and record your business expenses. FreshBooks expense tracking software lets you connect your business bank account so you can automatically import your expenses, saving you time and reducing the risk of manual error. In addition to automatic expense importing, you can also scan and organize receipts to make tax time a breeze.

3. Choose an Accounting Method

When it comes to accounting methods for entrepreneurs, you have two options to choose from. Once you choose your accounting approach, you’ll want to stay consistent with that method to make things easier when you file your taxes. The two types of accounting methods are:

- Cash-Basis Accounting: Cash basis accounting is the more straightforward of the two methods. It involves recording revenue when you receive the payment and recognizing expenses when you pay them. It’s the most popular option among new entrepreneurs because of its relative simplicity.

- Accrual-Basis Accounting: Under the accrual accounting method you record revenue when it’s earned and expenses when they’re incurred rather than when cash is actually exchanged. It gives a better reflection of your business’s overall income versus expenses than the cash accounting method gives, as it appropriately matches your revenue with your expenses.

4. Develop a Bookkeeping Method

Next, you’ll want to make sure your books are in order by adopting a consistent bookkeeping method for your business. The bookkeeping process involves tracking all your business transactions, from the revenue you earn to the expenses you incur. You’ll need to develop a bookkeeping method that you can stick with, so that you’re able to track all the money coming into and going out of your business. Here are some options for bookkeeping methods:

- DIY Bookkeeping: When you’re starting out as an entrepreneur, you might be able to get away with tracking all your business transactions using a spreadsheet. However, it may be worthwhile to invest some time into learning how to become an effective bookkeeper so you can more fully understand your small business finances. If you are interested in becoming a bookkeeper follow our guide on How to be a Bookkeeper. However, as your business grows, you might not have the time to manage all your bookkeeping manually.

- Cloud-Based Solution: For a small fee, you can subscribe to a cloud-based accounting software that can help you manage your bookkeeping services online and can even connect to your business bank account to track transactions automatically.

- Part-Time Bookkeeper: If you don’t want to worry about your bookkeeping and prefer to outsource the job to someone else, you can hire a part-time bookkeeper to manage the workload for you. Bookkeeping services can prepare financial statements, reconcile accounts, advise you on your taxes, and provide other day-to-day financial support that’s key to running your small business.

- In-House Bookkeeper: If your business grows to the point where bookkeeping becomes a full-time obligation, you can opt to bring on a full-time bookkeeper in-house.

5. Track Your Expenses

As an entrepreneur, you’ll need to track all your business expenses to create an organized record for tax season. It’s important that you develop a filing system for all your receipts and other paperwork, either by storing physical copies or developing a digital filing system.

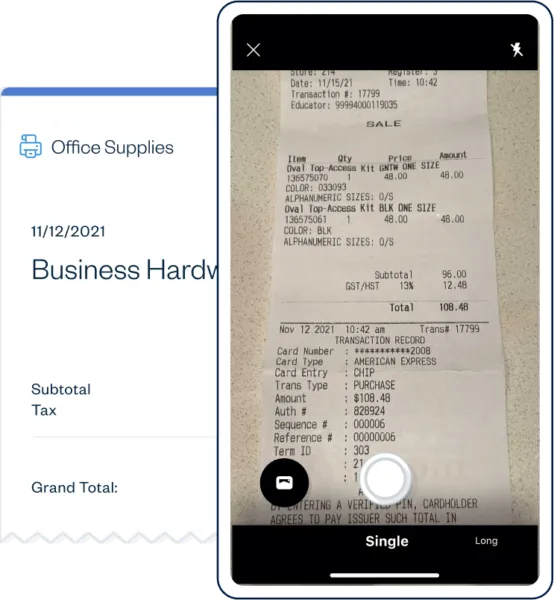

You can streamline your business expense tracking with FreshBooks expense and receipt tracking. Scan and digitize receipts, auto-capture important information, connect your bank account, and automatically import expenses for an all-in-one expense tracking solution. You can also categorize expenses so you can easily access all your important information for tax season. FreshBooks expense and receipt tracking helps you reduce clutter and organize your expenses so you never miss another deduction.

Some of the paperwork you’ll want to track includes:

- Bank and credit card statements

- Receipts from business meals, parking, travel, supplies, equipment, etc.

- Office bills, including utilities, internet, phone, etc.

- Financial statements

- Tax returns

For a full list of the records you should file as an entrepreneur, visit the IRS website.

6. Pick Your Payment Methods

Once your business is off the ground, it’s time to get paid for your hard work. To do so, you’ll need to decide which payment methods you’ll accept from your clients. If you’re just starting out, you can stick to simpler payment methods like checks and cash. But if you offer more flexible payment options, you may find that your clients pay you faster. Here are some options to consider:

- Credit Card Payments: If you have a brick and mortar shop, you may wish to set up a point-of-sale (POS) system and accept credit and debit payments in person. Keep in mind you’ll have to pay transaction fees every time a customer pays with a credit card, but the convenience and flexibility are often worth the cost.

- Mobile Payments: Mobile payment providers like Square are a great app option for entrepreneurs who conduct their business outside of an office. You’ll get a mobile card reader that attaches to a smartphone and pairs with an app to accept payment from anywhere with an internet connection.

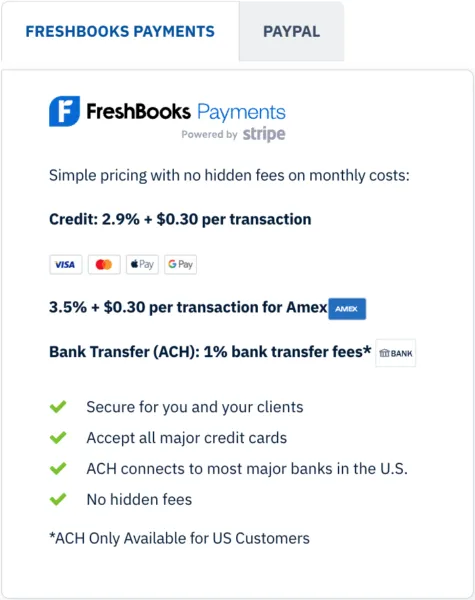

- Online Payments: Online payments are a convenient payment option that enables clients to pay from their digital devices. FreshBooks Payments powered by Stripe, offers an easy all-in-one payment solution so you can send your invoices and receive payment online. Accept credit, debit, Apple Pay, and bank transfers, send invoices with custom payment links, and receive payments in minutes through a secure and trusted system.

Also Read: How to Set Up Online Payments for Small Business

7. Learn Your Tax Obligations

As an entrepreneur, filing your taxes can be a bit daunting, especially if you’ve never done it before. Your tax obligations will depend on how your business is registered, since the requirements for a sole proprietorship are quite different from those of a corporation. Here are a few key tax obligations you’ll want to prepare for as an entrepreneur:

- Self-Employment Tax: All self-employed workers need to pay the self-employment tax to cover your Medicare and Social Security obligations. This is reported on your personal 1040 tax return in Schedule C.

- Employment Tax: If your business has employees, you’ll need to pay employment tax according to the Federal Insurance Contributions Act (FICA), to contribute to your employees’ Medicare and Social Security coverage.

- Income Tax: The income tax you file will depend on how your business is set up. If you run a sole proprietorship, you can file your business taxes as part of your personal income taxes. If you own a corporation, you’ll need to file separate tax returns for your company.

- Sales Tax: The sales tax you’ll need to charge clients and collect for the government is determined at the state level. Do your research to find out how much sales tax you need to collect and how often you need to submit it to the government.

8. Master Financial Reporting

Financial reports are crucial for entrepreneurs because they track how your business is performing. They can help you make informed decisions about the future of your company and show you how to become more efficient. The major financial statements entrepreneurs should be familiar with are:

- Income Statement: An income statement shows the revenue, expenses and ultimately the amount of profit or loss generated by a business, for a specific reporting period.

- Balance Sheet: The balance sheet reports a business’s assets, liabilities and equity at a specific point in time. In other words, it shows what a company owns and what it owes on a single day.

- Cash Flow Statement: Your cash flow statement offers a summary of the cash and cash equivalents coming into and going out of your business.

Financial reporting software makes it easier than ever to generate accurate financial reports for your small business. Access a wide variety of essential information including spending breakdowns, profit and loss reports, expense reports, and accounting reports so you can assess your company’s financial health at a glance and share information with investors. Review your business’s financial status and develop strategies to boost profits with this versatile reporting software.

What are the Benefits of Accounting for Entrepreneurs?

As an entrepreneur, proper accounting can help you better understand your business’s financial health and make informed decisions about your company’s finances. Here are some of the main benefits of proper accounting techniques for entrepreneurs:

1. Budget for Expenses

Accounting can help entrepreneurs create and manage detailed budgets for their businesses. When you understand how much money is coming into and going out of your business, you’re better equipped to plan for your expenses.

2. Improve Efficiency

With a proper accounting system in place, entrepreneurs can forecast revenues for their businesses. You’ll be able to see how efficiently your company generates revenue from your expenses. With that information, you can evaluate your marketing efforts to invest in campaigns that drive revenue and abandon those that don’t.

3. Simplify Tax Season

Accounting helps entrepreneurs prepare for tax season, to ease the headache of filing income taxes. With proper accounting and bookkeeping, you’ll have all the records of your business’s earnings and expenses organized which will make filing your income tax quicker and easier.

4. Monitor Your Growth

Accounting gives you a handle on your company’s assets and liabilities and how they change over time, which lets you monitor the growth of your business. You can understand what services are driving the most revenue in your business, which can help you adjust your business model to further grow your profits.

Enhance Your Accounting with FreshBooks

Developing a reliable accounting system for entrepreneurs is key to monitoring your company’s financial health and creating effective business strategies. It’s also a valuable way to share financial information with investors and shareholders so you can grow your business.

FreshBooks accounting software offers a straightforward way for entrepreneurs to manage their own accounting. Features like expense tracking and reporting help you manage your spending, while time tracking and invoicing make it easy to bill your clients. Try FreshBooks free to discover how the right accounting software can provide you with the tools to manage your business accounting.

FAQs About Entrepreneur Accounting

Learn more about how entrepreneurs use accounting and financial statements and when to prepare income statements with frequently asked questions about entrepreneur accounting.

How do entrepreneurs use accounting?

Entrepreneurs use accounting to create and track business budgets, develop growth strategies, and generate financial reports to attract potential investors. Accounting is also essential for the day-to-day management of cash flow and expenses, and for preparing the necessary information to file business taxes.

How do entrepreneurs make use of financial statements?

Entrepreneurs use financial statements to track the financial health of their business. This is necessary for ensuring that there’s adequate cash flow to run the business, for tracking expenses, and for assessing profits. They can also use financial statements to share information with potential investors and shareholders.

Which financial statement is most important for an entrepreneur?

One of the most important financial statements for an entrepreneur is the income statement, which tracks incoming and outgoing funds. This enables entrepreneurs to compare revenue and expenses and ensure that their business is making enough money to operate successfully. It’s also useful for developing strategies to reduce expenses and increase growth.

Should an entrepreneur prepare a cash flow statement?

Yes, an entrepreneur should prepare a cash flow statement. Tracking cash flow is important for monitoring the financial health of your business, anticipating potential cash flow challenges, and developing strategies to manage cash flow to help grow your business.

When should entrepreneurs prepare income statements?

Entrepreneurs should prepare income statements on a monthly or quarterly basis. For newer businesses, it’s generally recommended to prepare income statements at least every month so you can anticipate any potential challenges and adjust your strategy. For larger or more established companies, you may choose to only prepare quarterly income statements.

About the author

Michelle Payne has 15 years of experience as a Certified Public Accountant with a strong background in audit, tax, and consulting services. Michelle earned a Bachelor’s of Science and Accounting from Minnesota State University and has provided accounting support across a variety of industries, including retail, manufacturing, higher education, and professional services. She has more than five years of experience working with non-profit organizations in a finance capacity. Keep up with Michelle’s CPA career — and ultramarathoning endeavors — on LinkedIn.

RELATED ARTICLES

What Is a Journal Entry in Accounting?

What Is a Journal Entry in Accounting? What Is the Difference Between Cash and Accrual Accounting?

What Is the Difference Between Cash and Accrual Accounting? Single-Step vs Multi-Step Income Statement: Key Differences for Small Business Accounting

Single-Step vs Multi-Step Income Statement: Key Differences for Small Business Accounting How to Calculate Manufacturing Overhead Costs

How to Calculate Manufacturing Overhead Costs Business Budget: How to Create It in 6 Simple Steps

Business Budget: How to Create It in 6 Simple Steps 7 Questions About How Accounts Receivable Financing Works

7 Questions About How Accounts Receivable Financing Works