Modified Accelerated Cost Recovery System (MACRS) Depreciation

There can be a lot to know and understand when it comes to taxes. To help, we created this guide that breaks down everything you need to know about a modified accelerated cost recovery system (MACRS). Read on to learn more, including how it works, the different types, and the pros and cons!

![]() Table of Contents

Table of Contents

KEY TAKEAWAYS

- Using the modified accelerated cost recovery system (MACRS) allows you to recover the capitalized cost of an asset over a specific period.

- MACRS creates an opportunity for quicker depreciation earlier in an asset’s life, slowing down at a later period.

- There are guidelines outlined by the IRS for MACRS that provide estimates for the useful life of an asset.

- There are two primary types of MACRS systems. These are the Alternative Depreciation System (ADS) and the General Depreciation System (GDS).

What Is a Modified Accelerated Cost Recovery System (MACRS)?

A modified accelerated cost recovery system (MACRS) is a way to depreciate tangible and intangible property for tax purposes. When you own property that you will be using in your business for a year or more, the U.S. tax code allows you to recover the costs with annual tax deductions known as depreciation. MACRS includes two different systems to depreciate the property. One of the systems is the General Depreciation System (GDS) and the other is the Alternative Depreciation System (ADS). Each of the systems uses a different method and cost recovery periods to calculate the depreciation.

How the Modified Accelerated Cost Recovery System (MACRS) Works

When using MACRS, the first thing to do is determine the class that the business asset will fall into. This will allow you to see the exact number of depreciation years that are allowed within both the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). You will also have to determine when the property was placed in service, so you can determine the convention. The convention is important, because an asset placed in service in April will have a different cost recovery percentage for the first and last year of the asset’s life than one placed in service in September.

You might have certain office equipment, such as a printer, that could qualify for up to 5 depreciation deductions years under GDS. Once you find this information you’re going to develop a depreciation schedule. To do this, you simply find the appropriate depreciation rate from the depreciation tables provided by the IRS and multiply it by the base of the equipment to be depreciated.

What Are the Types of Modified Accelerated Cost Recovery System (MACRS)?

Within MACRS, there are two primary systems used. These are the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). The IRS will determine the total number of years that can get deducted, which is based on the class or type of property purchased.

The number of years the IRS assigns will depend on whether you use GDS or ADS. The primary difference between the two types of systems is that GDS has shorter depreciation periods and can offer three types of depreciation. ADS often has longer depreciation periods.

Furthermore, MACRS provides three depreciation methods under GDS and one depreciation method under ADS. The methods are:

- The 200% declining balance method over a GDS recovery period.

- The 150% declining balance method over a GDS recovery period.

- The straight line method over a GDS recovery period.

- The straight line method over an ADS recovery period.

The proper method is determined by looking at the type of property and when it was placed in services.

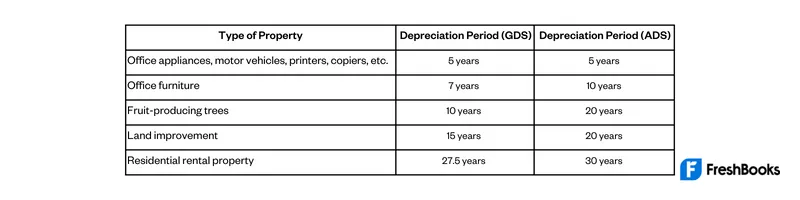

Here are examples of some of the most common types of property and their depreciation period:

Generally, most business properties will use GDS. With that said, you’re required by the IRS to use ADS if you have the following types of property:

- Properties that are tax-exempt and bond-financed

- Specific types of farming properties

- Nonresidential and residential property held by an electing real estate business

- A farming business property that uses GDS with a recovery period of 10 or more years

- Property used mostly outside of the United States

Pros and Cons of Modified Accelerated Cost Recovery System (MACRS)

One of the biggest things to consider when looking into MACRS is which deprecation system will work best for your business. It’s all going to depend on the type of property purchased. That said, here are some of the biggest pros and cons of MACRS.

Pros

- Designed to accelerate depreciation expenses for tax purposes

- Businesses can recognize a smaller amount of taxable income in the short term

- Provides businesses with more opportunities to invest in capital assets

Cons

- MACRS isn’t used on the financial statements of a business

- Many businesses use the straight-line method of depreciation or accelerated depreciation calculations

- It can result in discrepancies between the book basis and tax basis of the fixed assets of a business

Example of Modified Accelerated Cost Recovery System (MACRS)

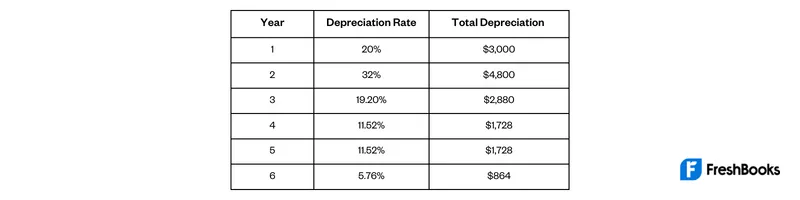

Let’s say that you purchase a new printer and copier for the office at the beginning of January for $15,000. After you find the right IRS depreciation table, you can start to fill in some information and do some calculations.

Here is what the table would look like, including depreciation percentages and calculations using the half year convention based on the initial $15,000 cost:

After the sixth year has finished, you would have recovered the initial total cost of the printer and copier at $15,000. Ultimately, you wouldn’t be able to deduct additional depreciation costs any further.

Summary

Calculating depreciation can often be a tedious and complicated process to undertake. But understanding how it works and maximizing the benefits can make a huge difference when it comes to tax time. MACRS is specifically designed to help lower total business tax liability.

It’s the only method that the IRS allows for tax purposes. The two main systems used within MACRS are the general depreciates system (GDS) and the alternative depreciation system (ADS).

FAQs About Modified Accelerated Cost Recovery System

Generally, MACRS applies to property in service after 1986. ACRS relates to property in service from 1981-1986.

You will need to know the basis, the property class, the depreciation method, and the depreciation convention. Then, you will need to find the right IRS depreciation table and percentages. Finally, you multiply the cost of the property by the depreciation percentage.

The straight-line method requires you to claim the same amount of tax every year until the asset’s useful life ends, whereas MACRS uses various methods like the Double Declining Balance.

The IRS outlines certain MACRS tables based on the type of property and depreciation method. The IRS website provides a complete breakdown of what you need to know.

Share: